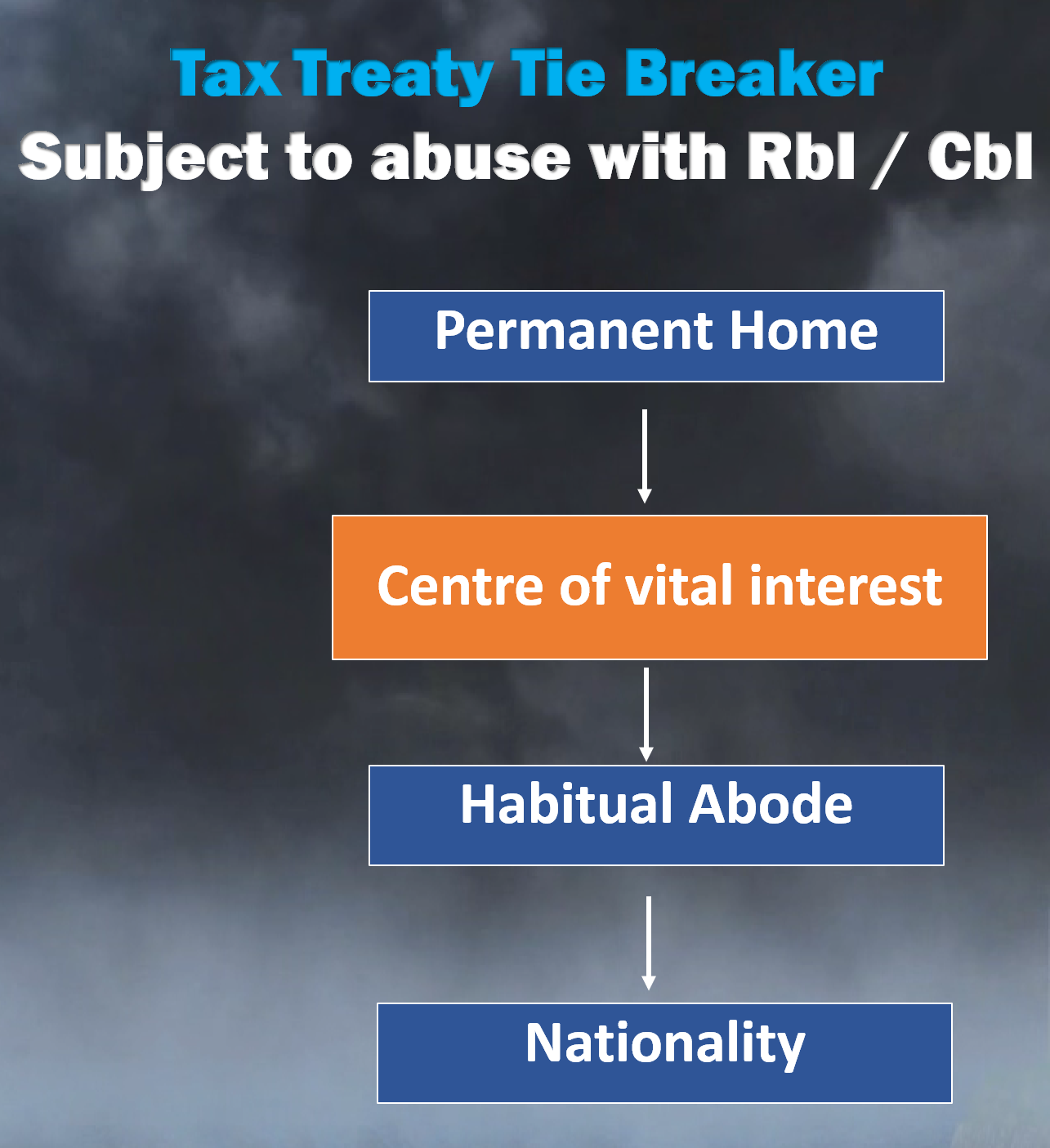

Tie Breaker Rule in Tax Treaties

Por um escritor misterioso

Descrição

Hello Connections, Let’s briefly discuss the Tie Breaker Rule in Tax Treaties. Tie Breaker Rule are used when an individual becomes resident in both contracting states due to their domestic laws/rules, to determine the residential status of such individual for the purpose of taxability of income.

Chapter 8 Are Tax Treaties Worth It for Developing Economies? in: Corporate Income Taxes under Pressure

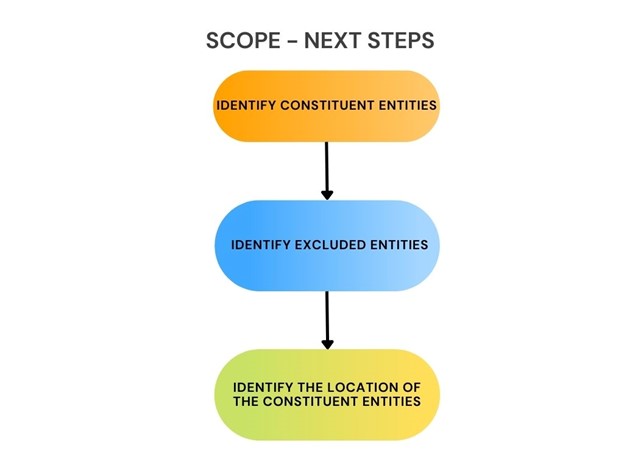

Identify Constituent and Excluded Entities »

International taxation - Wikipedia

How To Handle Dual Residents: IRS Tiebreakers

The Tax Times: LB&I Adds a Practice Unit Determining an Individual's Residency for Treaty Purposes

Closer Connection Test or a Treaty Tie-Breaker Provision

Relief Under Section 90/90a/91 of Income Tax Act, DTAA

Navigating Tax Treaties: Insights from IRS Publication 519 - FasterCapital

Residency under Tax Treaty and Tie Breaker Rules

How To Handle Dual Residents: The I.R.S. View On Treaty Tie-Breaker Rules - - United States

de

por adulto (o preço varia de acordo com o tamanho do grupo)