Eurozone Crisis and Banks' Creditworthiness: What is New for Credit Default Swap Spread Determinants? - Alessandra Ortolano, Eliana Angelini, 2022

Por um escritor misterioso

Descrição

Eliana ANGELINI, Università degli Studi G. d'Annunzio Chieti e Pescara, Chieti, UNICH, Department of Economics

Alessandra ORTOLANO, Research Assistant, Tuscia University, Viterbo, Tuscia, Department of Economics, Engineering, Society and Business Organization - DEIM

Risks Special Issue : Credit Risk Management

Eliana ANGELINI, Università degli Studi G. d'Annunzio Chieti e Pescara, Chieti, UNICH, Department of Economics

Eliana ANGELINI, Università degli Studi G. d'Annunzio Chieti e Pescara, Chieti, UNICH, Department of Economics

Linear regression of firm-level log average loan amount (y-axis) on log

Moving decomposition of the R2

Risks Special Issue : Credit Risk Management

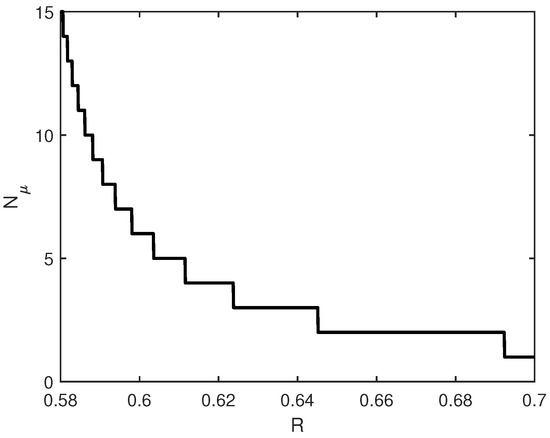

PDF) Credit Risk Management of Property Investments through Multi-Criteria Indicators

Risks Special Issue : Credit Risk Management

Risks, Free Full-Text

The final weight of sub-criteria in three banks

Pairwise scatter plots in the aggregate level

de

por adulto (o preço varia de acordo com o tamanho do grupo)